Soil health through the lens of the tech stack

This Seana Day post was a recent guest article on AgFunder News.

Seana is a partner at Culterra Capital and Venture Partner at Better Food Ventures, and is based in Turlock, California. Thanks to Rob Trice of Better Food Ventures and The Mixing Bowl for his contributions to this piece.

Interest around carbon capture in farmland soil has grabbed headlines since the 2018 Farm Bill in the US included provisions aimed at promoting soil health. Amplified by Indigo Ag’s launch of its own carbon marketplace, together with a host of other soil carbon innovators, the stage was set for a fresh agtech boom.

Like many, I am both intrigued and apprehensive about the carbon sequestration landscape. From taking a valid soil sample on a farm to compensating a farmer for sequestering carbon, there is a great deal of complexity.

The growing number of players in the soil carbon ecosystem and the numerous, shifting supply and demand drivers make this sector even harder to track.

To unpack the ecosystem and supply-demand drivers, I felt I needed a framework to understand where the players fit, how the data actually flows, and areas of friction to overcome.

As a recovering investment banker in the communications and wireless sector, I routinely look at emerging technology ecosystems through the lens of the open systems interconnection (OSI) model. Basically, the OSI model is a conceptual graphic representing interoperability functions in a telecom or computing system. It is illustrated as a vertical stack, with basic communications sitting at the lowest level and user interface at the highest level.

With that as a reference point, over the years my colleagues and I have often utilized this vertical tech stack concept to assess tech maturity and investability across various agtech sub-sectors.

And now, with the recent fervor and evolution within the carbon market, I am sharing my analysis with the broader industry to help frame the current state of soil health technology through the vertical tech stack lens.

As we wrote extensively in US Farmers and Ranchers in Action’s Transformative Investment in Climate Smart Ag report, there still exist myriad barriers to scaling up the adoption of climate-smart, soil-centric agriculture practices, including technology itself – so I will not delve into those specific barriers here.

Rather, I will focus specifically on the tech framework needed in order to accurately compensate farmers and ranchers for demonstrating soil health improvement through verifiable measurements and methods.

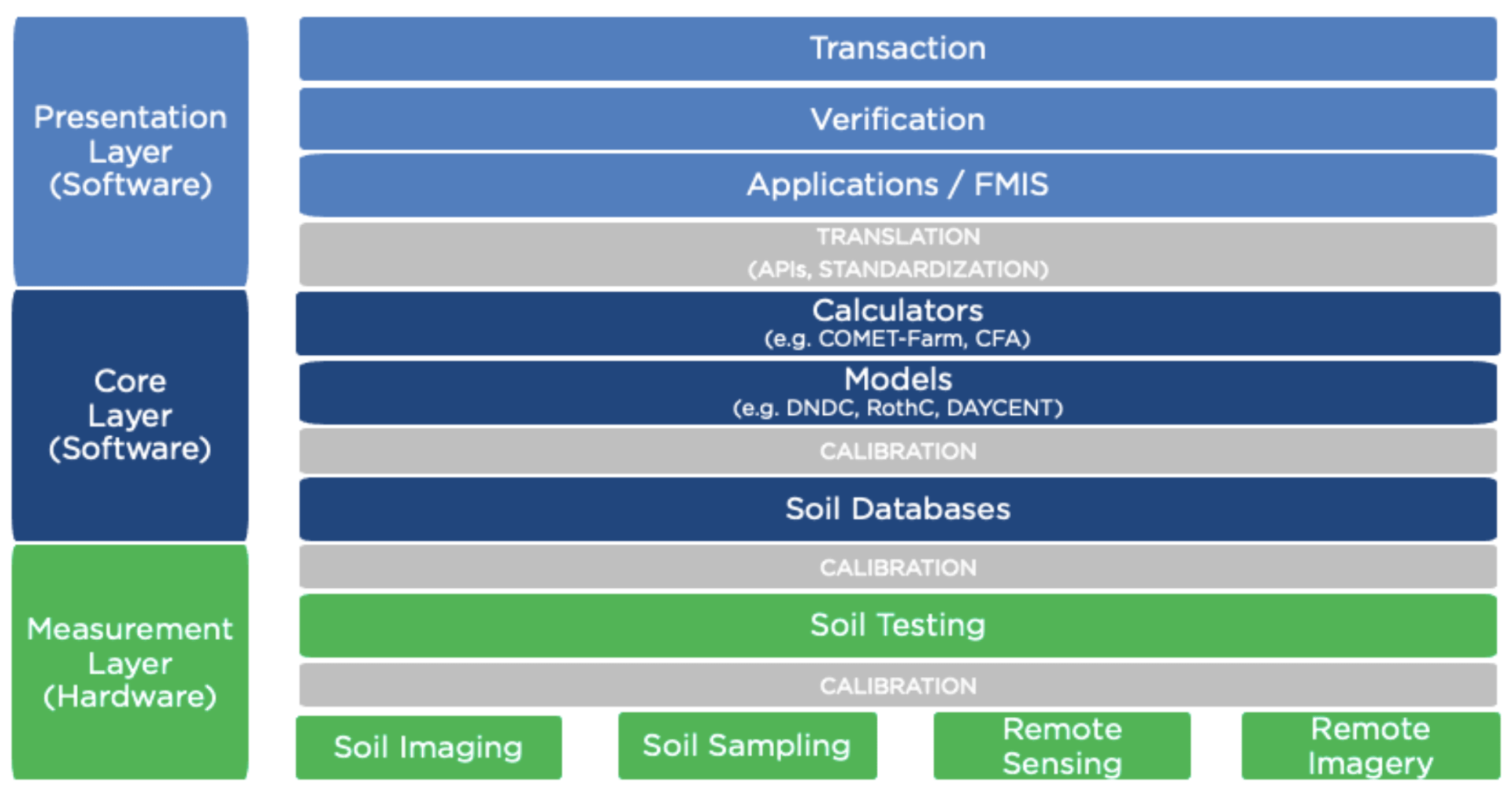

Culterra Capital’s Soil Health Tech Stack

Image credit: Culterra Capital

The Culterra Capital Soil Health Tech Stack (image above) illustrates the interdependence of technology, science, and economics in connecting suppliers of soil carbon credits and soil health outcomes to buyers.

Setting the foundation

The ‘core layer’ (dark blue) of the Soil Health Tech Stack is the digital representation of the source data (eg, soil measurement) that underpins the validity of, and confidence in, the value of soil carbon credits or other soil health outcome-derived compensation.

This is where environmental science lives in soil databases, carbon sequestration models, soil health models, and so on. It requires continuous feedback loops, long-term research, pre-competitive partnerships, and a lot of collaboration.

Prior to embarking on this soil tech learning journey, I didn’t appreciate how much calibration and translation was still needed to make data flows work in the Soil Health Tech Stack.

The grey layers on the graphic represent the places where data must be calibrated before it is fed into the next layer. Today there are substantial gaps in soil measurement and analytical tool calibration that still need to be addressed.

Calibrating the collection

The bottom ‘measurement layer’ (green) is still quite nascent. Most soil sample collection on farms today is done by someone — like a high school student getting paid by the hour — pushing an old-fashioned soil probe into the ground and scraping a sample into plastic baggies that are labelled and sent through the mail to a corporate or university soil lab.

Until recently, most innovation in the measurement layer has been driven primarily by hardware companies that are easing the cost, burden, and potential variability of soil data collection. Many of these hardware companies are heavily software-enabled with sophisticated analytics that leverage existing soil databases.

“Revealing the best investment opportunities across the food supply chain – read more here”

In the past few years we have seen more innovation in the measurement layer coming from remote sensing. whereby aerial platforms (eg, drones, aircraft, and satellites) gain insights on soil through hyperspectral sensors. Remote sensing, of course, is less manual and more cost effective but will not be as capable of analyzing all the aspects of soil as an in situ sensor.

The holy grail in soil health will be integrating enough ground-truthed soil measurements to feed robust data models that are powered by machine learning and artificial intelligence (ML/AI) to interpolate the soil health of a particular farm field, pasture, paddock, or range land. In this way, remote sensors can be used in lieu of field-based measurement for verification.

Whether the market will ultimately arrive at a ‘measure-plus-model,’ ‘model-only,’ or ‘measure-only’ approach, it is too early to tell. But the potential power of ML/AI to improve model accuracy is clear. The value in robust modelling both accelerates scenario planning and calibration, and lowers the cost of soil measurement, reporting, and verification (MRV) – all of which are key to growing the market as well as confidence in the outcomes.

Monetizing the measurements

The ‘presentation layer’ (light blue) is really where the measurement and model data is monetized for soil health outcomes. To date, this is where the majority of startup funding and preliminary value has been concentrated in the soil carbon market boom.

My cautionary note after doing a deep dive into the soil health tech landscape is that most of the focus and capital has been accumulating at the presentation layer. While these companies have shown they can move at the speed of tech and harness talent and capital looking for transformative, climate-smart opportunities, we also need more of those resources to close the calibration gaps at the measurement and core layers.

In order to realize a viable long-term market for soil health and soil carbon at scale, we need to prioritize the digital ag flywheel which will support broader data collection, analysis, feedback, and overall adoption to enable the full Soil Health Tech Stack.